Your score quantifies how much of a risk you are to a potential lender. A

What’s your credit score? Negative news Getting credit Getting your report How to keep your credit score in good shape in bad times

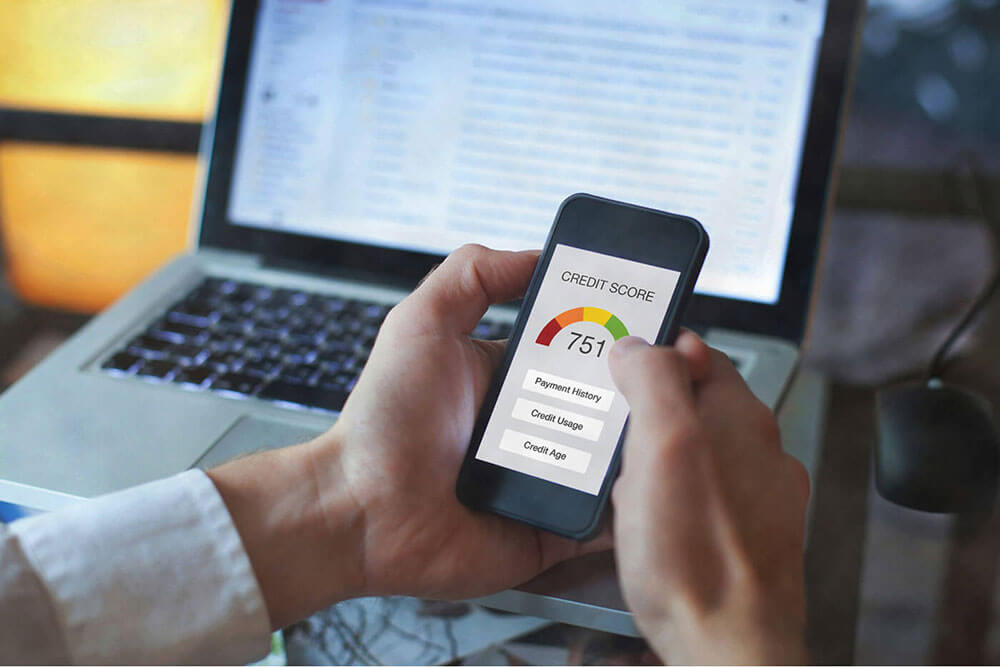

What’s your credit score?

Your

- Make payments on time—even if it’s only the minimum.

- Contact your lender as soon as possible if you’re unsure about being able to pay a bill.

- Even if a bill is in dispute, pay it.

- The longer your credit history, the better. Keep old credit card accounts active by using them occasionally. (Make sure they don’t carry a fee.) If you are tempted to transfer your current balance to a new card to take advantage of a promotional fee, remember that the

new account is considered new credit with no prior history.

Negative news

Getting credit

- Apply for credit when you are in good financial shape. Even if you don’t need it, you can keep the firepower in case of a rainy day. But there can be too much of a good thing.

- Use less than 35 per cent of the credit available. Add up all the credit available to you on credit cards, lines of credit, and loans, then multiply by 35 per cent. Avoid using more than this at one time. Even if you pay all your balances in full by due dates, lenders see you as higher risk if you are using most of your available credit.

- Each time you apply for a credit card or loan, or even a rental apartment or new job, it triggers a credit check or inquiry. The more inquiries on your record, the worse your score, since lenders may assume you are strapped for cash or that you are using credit to live beyond your means. (Requesting your own credit report does not count as an inquiry.) If you are shopping around for the best rates on a mortgage or car loan, try to do this within a two-week period as it will count as one inquiry. Moving to a new city incurs applications for mortgages, utility, cable and phone accounts, and even these inquiries deduct points for your credit score!

Diversify your credit . Having multiple sources of credit, such as a mortgage, car loan, credit card, and line of credit is better for your score than having one large loan. Just make sure you keep track of the payment due dates to avoid being in arrears.

Getting your report

- Credit reports are available from credit monitoring bureaus such as

Equifax Canada orTransUnion Canada , and sometimes for free. Read the fine print to ensure that you haven’t signed up for a paid service. - Before you provide any personal information, double-check that the website url says https, not http.

- Check for errors on your report, such as a wrong address or birthdate, incorrect loan amounts, and especially any negative information about accounts past the maximum number of years such information is allowed to stay on record. If your report contains accounts that you did not open, it could be a sign of identity fraud. Report this immediately to Equifax Canada and TransUnion Canada, as well as the Canadian Anti-Fraud Centre, and request that a fraud alert be placed on your credit report.

- In times of economic turmoil, it may be difficult to make all your payments. Because of current circumstances, banks and other lenders have announced programs to defer payments for those who are facing financial difficulty. Before you take advantage of these offers, ensure you understand what the implications are for your credit score and get any commitments to have a payment deferred

in writing . Don’t just take the word of the customer service rep on the call.

How to keep your credit score in good shape in bad times

- Make the minimum payment. If you are carrying a balance on a high-interest credit card, consider getting a line of credit (with a much lower interest rate) to pay off your card.

- Contact your lender and ask for a payment deferral or payment holiday. You will still be charged interest but will not have to pay down the principal. Contact a credit monitoring bureau first to confirm how this would affect your credit score.

- Your mortgage lender will likely be willing to help you in a variety of ways, such as extending the amortization period to lower your monthly mortgage payments, adding any missed payments to your balance, reducing your payments for a certain period, converting a variable interest rate to a fixed one in case interest rates shoot up.

Credit is a great tool to provide a buffer in emergencies, as well as giving you more investing options—just make sure you use it well.

Rita Silvan, CIM™️, is personal finance and investment writer and editor. She is the former editor-in-chief of ELLE Canada magazine and is an award-winning journalist and tv media personality. Rita is the editor-in-chief of

Golden Girl Finance , an online magazine focusing on women’s financial success. When not writing about all things financial, Rita explores Toronto’s parks with her standard poodle.